By Zoe A. Zurn, Associate, Chicago

Macroeconomic uncertainty has complicated business valuations as inflation, interest rate volatility, tariff pressures, and data gaps challenge forecasting and weaken investor and consumer confidence. Valuation professionals may adjust assumptions and methodologies to produce credible and defensible valuation conclusions amid ongoing uncertainty.

Introduction

Macroeconomic uncertainty has become a defining feature of today’s business environment, reshaping how valuation professionals approach their work.

Through 2025 and into early 2026, persistent inflation between 2.3 percent and 3.0 percent, interest rate volatility, and fiscal gridlock, including a record 43-day government shutdown, amplified uncertainty. The absence of key economic data, combined with tariff-driven price pressures and labor market softening, has complicated forecasting and valuation assumptions.

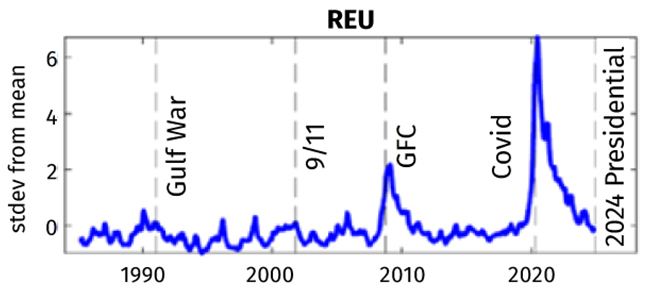

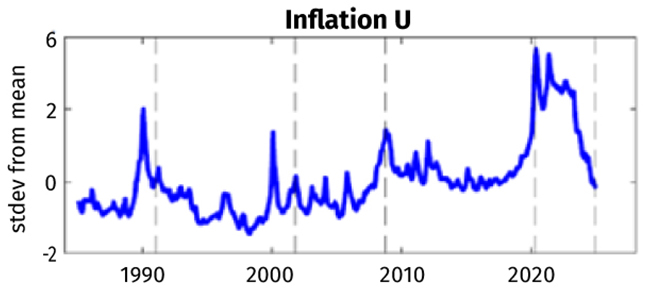

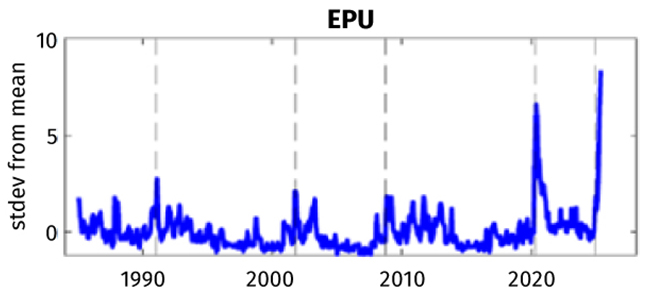

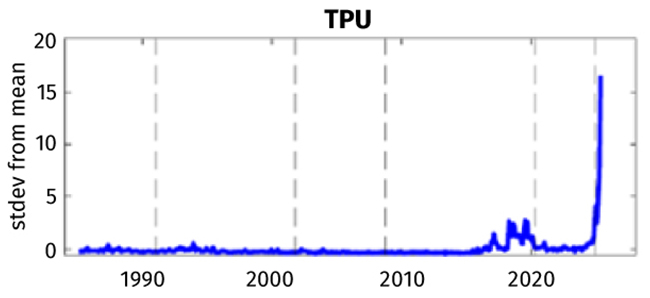

The Federal Reserve (the “Fed”) tracks six critical measures: real economic uncertainty (“REU”), inflation uncertainty (“Inflation U”), economic policy uncertainty (“EPU”), trade policy uncertainty (“TPU”), geopolitical risk (“GPR”), and market volatility as measured by the CBOE Volatility Index (“VIX”).1 These metrics, when levels are high, can lead to delayed investment, cautious consumer spending, and tighter credit conditions.

For valuation professionals, heightened uncertainty drives up equity risk premiums and borrowing costs, which might increase a company’s weighted average cost of capital (“WACC”) and, all else being equal, result in a lower business valuation.

In this environment, adaptive methodologies and transparent communication help to maintain credibility and guide clients through volatile conditions.

Valuation Implications of Uncertainty

Macroeconomic uncertainty influences business valuation through several channels. Inflation and interest rate volatility affect discount rates and borrowing costs, while trade policy risks can disrupt supply chains and affect profit margins. At the same time, gaps in economic data and policy unpredictability undermine forecasting accuracy. The following sections explore these key drivers and their implications for valuation assumptions.

Inflation and Interest Rate Volatility

Ongoing inflation can increase the equity risk premium applicable in a business valuation, typically increasing the WACC and decreasing the business valuation. Elevated inflation also can raise input costs and operating expenses, which can compress margins and reduce projected cash flow if companies are unable to pass cost increases on to consumers.

High interest rates put downward pressure on business valuations primarily by increasing the risk-free rate, which is a foundation of most cost of equity capital models, including the modified capital asset pricing model, traditional capital asset pricing model, and the build-up model. When the risk-free rate increases, the required rate of return for equity investors often increases because investors demand higher compensation relative to the baseline return available on perceived risk-free securities. This results in a higher cost of equity, which typically raises the WACC and lowers the resulting discounted cash flow valuation, if other variables remain constant.

Despite recent rate cuts by the Fed, borrowing costs may remain elevated because investors require higher compensation for enduring uncertainty. Unlike risk, which involves known probabilities, uncertainty lacks a defined range of outcomes, making traditional risk models less effective in uncertain environments. Inflation and economic uncertainty oftentimes make financial institutions more risk-averse, leading to tighter lending conditions. Higher borrowing costs further constrain companies seeking credit for larger investments, influencing near-term operations and projected capital expenditures.

Heightened economic uncertainty regarding inflation and interest rates also generally compresses market valuation pricing multiples, such as price to earnings and enterprise value to earnings before interest, taxes, depreciation, and amortization, because investors demand higher risk premiums and stock prices fluctuate.

At the same time, deal activity tends to slow because rising borrowing costs make leveraged transactions less attractive, while uncertainty complicates the estimation of post-transaction synergies in strategic transactions. With fewer consistent comparable transactions and a wider range of observed multiples, it can become more difficult for a valuation professional to apply a market approach in the context of a business valuation.

Collectively, inflation, interest rate volatility, and broader economic uncertainty oftentimes increase required returns and reduce confidence in future cash flow, which can put downward pressure on income-based valuations and market pricing multiples.

Trade Policy and Tariffs

TPU adds another layer of complexity to valuation assignments. The current administration has emphasized the importance of tariffs to protect domestic production, raise tariff revenue, and negotiate foreign policy. However, levying significant tariffs on imported goods from primary trading partners can disrupt global value chains. International companies often hesitate to allocate capital to export-heavy contracts if trade barriers make their products more costly. The effects of TPU are more prominent in emerging and developing markets because a reduction in global demand reduces production, slows gross domestic product growth, and weakens the labor market through job cuts.

Regardless of whether businesses can absorb tariff costs or pass them on to customers, shifts in demand can materially affect revenue forecasts. Business decision-makers may struggle to quantify the effects of tariffs without knowing their duration or lasting effect on supply and demand. These dynamics make it critical for valuation professionals to consider and evaluate tariff-related risks when projecting cash flow to apply in a business valuation (e.g., in the application of the income approach, discounted cash flow method).

Data Gaps and Policy Uncertainty

Limited access to economic data, such as the gaps caused by the U.S. government shutdown in the fourth quarter of 2025, can undermine forecasting accuracy. Delayed or missing labor and inflation reports can leave policymakers and valuation professionals without critical inputs, leading to increased uncertainty around interest rate decisions and valuation assumptions. This uncertainty often translates into market volatility, further complicating the use of market data in valuation models.

The Fed decreased interest rates for the third consecutive time at its final meeting of 2025, prioritizing support for a weakened labor market over concerns about inflation. The decision to lower rates by a quarter-point was not unanimous—three members dissented—marking the first significant disagreement among Fed members in six years.

Officials remain divided on the appropriate policy path going forward as they continue to navigate decisions without access to complete economic data. Recent concerns suggest that headline job gains may have been overstated due to missed submissions during the shutdown. The Fed expects to have clarity in early 2026 when the Labor Department is expected to release delayed employment reports for October and November 2025, along with December figures.2

The absence of reliable economic data has a direct effect on valuation analyses. Policymakers depend on numerous inputs when making decisions that influence the broader economy, and valuation professionals similarly rely on accurate market data to estimate the WACC, establish terminal growth rates, and project free cash flow. Transparency in key assumptions and documentation remains important to support defensible valuation conclusions.

Industry-Specific Effects

Macroeconomic uncertainty affects the entire economy, but some industries are more vulnerable than others. Businesses that rely heavily on global supply chains often face the greatest exposure to factors such as inflation, tariffs, trade disruptions, and overall volatility.

For example, manufacturing faced substantial cost pressures recently because of trade tariffs. High levels of volatility forced many manufacturers into a “wait and see” approach, uncertain about future capital investments and earnings. Facing so many issues at once, manufacturing leaders have shifted their priorities from low-cost operations to low-risk operations. Companies that consider themselves to be industry leaders are prioritizing localization, which involves producing in the region where the end market resides. Localization can minimize the effects of trade tariffs. Some manufacturers anticipate a tariff-induced recession that might lead to demand instability in the market.3

Within retail, tariffs on imported goods have raised consumer prices, squeezing profit margins. In addition, broad economic uncertainty typically leaves consumers hesitant to spend. A softening job report often encourages the Fed to implement a rate cut; however, if upward price pressure is already in the economy, a rate cut might not help to combat inflation. This effect, known as stagflation, typically results in lower consumer spending.

U.S. Census Bureau advance estimates show that retail and food services sales were virtually flat in December 2025, falling short of expectations for a 0.4 percent increase.4 Sluggish holiday spending reflected weakening consumer demand as inflation and tariff-driven price increases continued to erode purchasing power amid slowing wage growth.

Such factors have caused challenges for business decision-makers, making it increasingly difficult to forecast business performance across various sectors and industries.

The Federal Reserve’s Perspective

Since 2019 (i.e., prior to the COVID-19 pandemic), key indicators of uncertainty have climbed to their highest levels in decades. As economic and financial uncertainty persists, researchers continue to examine how, and the extent to which, these elevated levels have significant and measurable effects on the broader economy.5

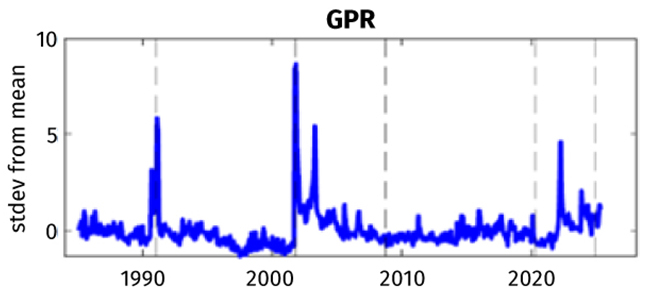

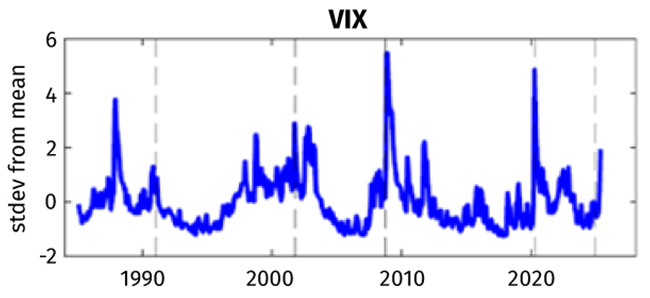

Figure 1: The Federal Reserve’s Key Metrics

Source: FEDS Notes.

The six key metrics measured by the Fed—(1) REU, (2) Inflation U, (3) EPU, (4) TPU, (5) GPR, and (6) the VIX—have become increasingly relevant in assessing the effect of shocks to uncertainty in today’s transformative business environment.

For context, the data in Figure 1 spans from 1985 to 2025, capturing major periods of heightened uncertainty, including the Gulf War, the 9/11 terrorist attacks, the 2008 Global Financial Crisis, the COVID-19 pandemic, and the 2024 presidential election.

As presented in Figure 1, TPU and EPU have seen the largest increases in recent years, with standard deviations above their respective historic means of approximately 16 and 8.3, respectively.

Across all measures of uncertainty, three consistent effects emerge: (1) delayed or reduced investment and hiring, (2) more cautious consumer behavior, and (3) tighter credit conditions. Businesses and households often adopt a “wait and see” approach, postponing major investments and purchases to preserve liquidity until economic conditions and the outlook become clearer.

One of the most widely used indicators of uncertainty is the VIX. The VIX measures expected 30-day volatility in the U.S. stock market, derived from mid-quote prices of S&P 500 Index call and put options. It serves as a barometer of global risk sentiment, signaling heightened uncertainty across financial markets.

Sharp spikes in the VIX are typically driven by market sentiment, liquidity constraints, and leverage cycles. In response, investors might reallocate capital toward safer alternatives, such as U.S. Treasuries. This shift often triggers capital outflows from emerging markets, leading to currency depreciation, inflationary pressures, and restricted access to credit. These effects are further amplified when central banks tighten monetary policy to stabilize currencies.

From a valuation perspective, elevated financial uncertainty reflected by the VIX can materially affect a company’s WACC. Rising market risk premiums increase the cost of equity, while tighter credit conditions and higher borrowing spreads raise the cost of debt. A company’s optimal capital structure might change, affecting levered company betas as an input for the WACC. Although debt is generally less expensive than equity, companies that have weaker credit profiles might lose access to debt financing and rely more heavily on equity, further driving up the WACC. A higher WACC reduces the present value of expected cash flow, all else being equal, ultimately lowering a business valuation.

Adapting Valuation Methodologies

Although valuation professionals cannot control macroeconomic uncertainty, thorough due diligence allows for adjustments that account for potential outcomes. A critical component of a robust business valuation is the set of assumptions underlying the valuation methodology. Although future cash flow cannot be predicted with certainty, each input, such as cost of equity, cost of debt, growth rates, or inflation, may be supported by empirical evidence and sound justification.

When addressing TPU, it is important to avoid double-counting risk factors. For example, if trade policy risk effects, such as reduced margins or lower expected revenue, are already reflected in cash flow projections, those risks then should not also be accounted for in the selected present value discount rate.

Conversely, if the magnitude of trade policy or tariff effects remains uncertain, adjusting the discount rate to capture broader risk may be appropriate.6 Clear documentation of assumptions and rationale can help maintain transparency and credibility.

Sensitivity analysis, a standard practice in many business valuations, is particularly effective during periods of heightened volatility. Expanding the range of sensitivities may be necessary to capture extreme scenarios because the extent of uncertainty remains unknown. Valuation professionals also can incorporate estimated scenario probabilities to calculate expected future values, providing a more nuanced view of potential outcomes.

Dynamic forecasting offers another way to mitigate uncertainty. Valuation analyses often rely on management-prepared forecasts, which can quickly become outdated in volatile environments. Encouraging clients to adopt rolling forecasts, updated monthly or quarterly, can help maintain relevance. Communicating the benefits of timely updates, setting expectations early, and documenting year-over-year trends or changes ensure assumptions remain current and valuations remain more supportable. This approach not only improves accuracy, but it also reinforces transparency and strengthens client relationships.

Ultimately, the most effective way to navigate macroeconomic uncertainty is through clear communication with the client. This practice enhances credibility and ensures compliance with recognized professional standards.

Professional standards issued by The Appraisal Foundation, the American Society of Appraisers, the National Association of Certified Valuators and Analysts, and the International Valuation Standards Council emphasize full disclosure in a valuation engagement.

Valuation professionals may thoroughly document the sources and rationale for key assumptions, as well as methodologies used to address uncertainty, such as sensitivity analysis, scenario modeling, and dynamic forecasting. Any limitations or constraints, including restricted access to economic or industry data, also may be disclosed to maintain transparency and uphold professional integrity.

Conclusion

Macroeconomic uncertainty has become a structural reality in today’s dynamic business, political, and economic environment. Navigating business valuations in this context requires innovative approaches and adaptive methodologies that go beyond traditional practices.

Valuation professionals can embrace thought leadership, providing strategic insight, transparent communication, and flexible solutions backed by empirical evidence and extensive research to address clients’ unique challenges and increasingly complex financial forecasts. By doing so, valuation professionals not only deliver credible valuations, but they also position themselves as trusted advisors during a volatile time.

About the Author

Zoe is an Associate at Willamette Management Associates, based in our Chicago office. She can be reached at (773) 399-4323 or zoe.zurn@willamette.com.

References:

- Juan M. Londono, Sai Ma, and Beth Anne Wilson, “Costs of Rising Uncertainty,” FEDS Notes (April 24, 2025), https://doi.org/10.17016/2380-7172.3779.

- The Federal Reserve, “Transcript of Chair Powell’s Press Conference” (December 10, 2025), 7.

- Roland Berger, “Navigating Uncertainty,” Manufacturers Alliance, (2025).

- U.S. Census Bureau, “Monthly Retail Trade Report” (February 10, 2026), https://www.census.gov/retail/sales.html.

- Londono, Ma, and Wilson, “Costs of Rising Uncertainty.”

- Frederik Bort and Marina Arias, “Tariffs and valuation,” KPMG (2025).